Home » Insight » US oil & gas – Will the success story continue?

During the second week of December 2023 we attended a so-called bus tour for investors organised by Scotiabank. We had management meetings in offices of 13 companies in Houston, USA including five upstream, three midstream / infrastructure, one refining and four integrated oil and gas companies. It was a very insightful trip, which provided us with a very good overview of the US oil and gas sector.

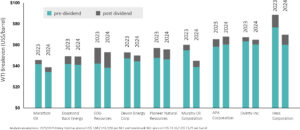

Overall all companies were optimistic and confident about their financial and operational position. They are all generating FCF (free cash flow) and the main question for them is how much and in what form to return capital to shareholders (predominantly through share buybacks), while managing assets in the most efficient way. The FCF business model is resilient so far and capital discipline is intact. The E&Ps and integrated companies all pointed out that they have flexibility to adjust capex in a weaker oil and gas price environment if it happens. The breakevens have not changed much from previous years. Going forward, the breakevens may even decrease or remain at current levels (Exhibit 1). The level at which companies would start to adjust their capital budgets varies, but $60 WTI was mentioned several times (that includes dividends and share buybacks).

Figure 1: 2023 and 2024 Free Cash Flow breakeven

Source: Marathon Oil investor presentation

Operating costs and inflation: the only item that is considered inflationary is labour because of a limited pool of available workforce in the industry. Other costs (steel, sand, other materials) are in a mild deflation and are expected to pull back by mid-single digit in 2024 (around -5%). Overall operating costs and unit capex should remain well under control.

Operational efficiencies are very robust and more durable than many expected. The efficiencies are realised above surface and subsurface:

Subsurface efficiencies are driven by big data analysis and machine learning (have been for several years), which for example enable companies to better select new locations or achieve better placement within zones being drilled.

The above surface efficiencies are driven by same technologies (e.g. analysing historical data and running thousands of simulations) and are enabling companies to cut drilling time and more efficiently use services to cut costs by for example managing timing of completions and fracking crews with drilling, to utilise completion and fracking crews 24/7.

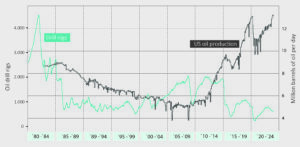

Drilling three-mile wells was discussed several times and all operators said they are implementing it: in essence, instead of drilling 2 x 1.5mile horizontal wells operators are now drilling one 3.0mile horizontal well, which reduces the overall cost by the cost of one vertical section (c. 15% of the total cost); the challenge with 3.0mile horizontal wells is productivity and recovery of hydrocarbons from the last mile of the horizontal section (it can be 25% lower from the last mile), but on balance this is cheaper and more effective than drilling two 1.5mile wells. This also has implications for rig count, which is falling while productivity and output in the US is growing (Figure 2).

Artificial Intelligence: in addition to machine learning and big data analysis generative AI is opening new and exciting opportunities to even further improve efficiencies (for example in deepwater exploration and drilling).

Figure 2: More oil from fewer rigs – US oil output has soared while drilling has declined

Source: Bloomberg, Baker Hughes, EIA

Inventory: several companies said ‘the sector has an inventory issue, but that is not the case for our company’, and with very impressive and robust operational efficiencies we think that drilling locations that were Tier-1 (in terms of IRRs) 5-10 years ago are being exhausted, but with more efficient drilling some of Tier-2 locations are moving into Tier-1 and replenishing Tier-1 inventory, so this may not be such an issue as perceived by the market. The Permian and in general US shale output is expected to be more gassy as the sector matures (higher Gas Oil Ratio). That is fully recognised by midstream companies which are planning for further growth of gas processing facilities and infrastructure enhancements where possible.

Output growth: while companies are not budgeting major output growth, and are remaining disciplined in capital allocation, the efficiency gains and low-single digit organic growth are altogether adding to a material growth for the sector overall. We have seen this year growth of around 850,000 barrels of oil per day (bopd) and some of the companies said that they expect overall US liquids growth in 2024 at similar levels to 2023. While this may not be fully recognised by the market yet, OPEC+ has already announced output cut in anticipation of higher supply and weaker demand. So, where is the limit for US output? Various sources have quoted 14-15million bopd as the current limit of infrastructure in the US, which is now producing 13.2milion bopd. With few more years of growth like we have seen in 2023, the US output could be reaching its capacity constraints. If this capacity limit is correct than new pipelines will be required for further growth, but will the US regulators approve them? The gas midstream companies we met are all planning for enhancements of existing infrastructure and facilities growth. Capacities are being booked now until 2025, but beyond that there is a need for new gas pipelines.

Consolidation: given recent large M&A deals in the sector this was one of the main questions in all meetings. While companies recognised advantages and importance of scale, several of them pointed out that it is more important to get better rather than bigger. We think the consolidation of the sector will continue, but it will be targeted to specific areas where material synergies can be achieved.

In conclusion, we think the US oil & gas sector has much more room for growth. The main impediment to that could be available infrastructure.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

Source: Bloomberg, Baker Hughes, EIA

Source: Bloomberg, Baker Hughes, EIA